How I Survived the Stock Market Rollercoaster and Found My Investment Soul

Ever felt your heart race as the market swings wildly while you clutch your phone, wondering whether to sell or hold? I’ve been there—burned by hype, lured by “sure bets,” and nearly gave up. But through trial, error, and real-world testing, I discovered a mindset that changed everything. It’s not about chasing quick wins; it’s about building a resilient approach that lasts. Let me walk you through what actually works. This journey isn’t about finding a magic formula or predicting the next big stock. It’s about creating a foundation that keeps you steady when emotions run high and uncertainty clouds judgment. For many women in their 30s to 55s, investing isn’t just about growing money—it’s about security, independence, and peace of mind for themselves and their families. The good news? You don’t need a finance degree or insider knowledge to succeed. What you do need is clarity, discipline, and a strategy rooted in reality, not hype.

The Moment Everything Changed: A Wake-Up Call from the Market

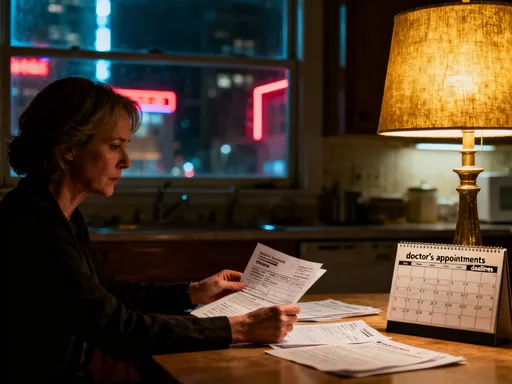

It was March 2020, and the world felt like it was unraveling. Markets plunged, headlines screamed crisis, and fear spread faster than facts. I remember sitting at my kitchen table, laptop open, staring at a portfolio that had lost nearly 30 percent of its value in just two weeks. My stomach tightened. I had followed what seemed like smart advice—diversified across tech, healthcare, and consumer stocks—but now everything was falling together. I had never felt so powerless. That morning, I almost clicked “sell all.” I was one impulsive decision away from locking in those losses for good.

What stopped me wasn’t wisdom—it was exhaustion. I had already made this mistake before. A few years earlier, during a smaller correction, I’d panicked and sold at the bottom, only to watch the market rebound months later. This time, I hesitated. I called a friend who’d stayed calm through past downturns. She didn’t offer stock tips or market predictions. Instead, she asked, “Do you know why you own these investments?” That question hit hard. I realized I couldn’t answer it clearly. I had bought based on recommendations, trends, and hope—but not a coherent plan. I didn’t have a strategy; I had a collection of hopes wrapped in stock symbols.

That conversation became my turning point. I decided to stop reacting and start understanding. Over the next few months, I stepped back from trading and focused on learning. I read books, reviewed my financial goals, and studied how different asset classes behaved over time. I learned that market drops, while painful, are part of the cycle—not signs of failure. More importantly, I discovered that my real enemy wasn’t the market; it was my own lack of direction. The market doesn’t punish investors for falling prices. It punishes those without a plan when prices fall. That realization shifted everything. I stopped chasing performance and began building a framework that could withstand volatility—because it was based on purpose, not panic.

Why Philosophy Beats Hype in Stock Investing

It’s easy to get caught up in the noise. One day, everyone’s talking about a hot new tech IPO. The next, a meme stock rockets higher on social media buzz. These moments create a sense of urgency—like if you don’t act now, you’ll miss out forever. But history shows a different story. For every investor who made a quick profit riding a speculative wave, countless others bought at the peak and held on as the bubble burst. Hype doesn’t build wealth; it erodes it. What lasts isn’t the latest trend but a clear, consistent philosophy that guides decisions regardless of market mood.

An investment philosophy isn’t a complicated theory or a secret formula. It’s simply your personal set of beliefs about how investing should work for you. It answers fundamental questions: What are you trying to achieve? How much risk are you comfortable taking? How long are you willing to wait? Without these answers, even the best-performing stocks can become liabilities. Imagine planting a garden without knowing what you’re growing or how much sunlight the plants need. You might water daily, but if you’ve planted shade-loving ferns in full sun, they’ll wither no matter how hard you try. The same is true with money. You can follow every tip and trend, but without alignment to your goals, your portfolio won’t thrive.

Consider the rise and fall of meme stocks around 2021. Some investors made life-changing gains in days. But many who joined late paid steep prices, only to see values collapse weeks later. Those who survived weren’t necessarily smarter—they were clearer. They had decided in advance what portion of their portfolio, if any, they’d allocate to speculative bets. They set limits and stuck to them. Meanwhile, others got swept up in emotion, risking retirement savings on unproven companies with no earnings. The difference wasn’t access to information; it was having a philosophy that acted as a filter. When excitement builds, a strong philosophy doesn’t shout louder—it holds the line. It reminds you that wealth isn’t built in a sprint. It’s grown steadily, over time, with intention.

Building Your Core Strategy: Clarity Before Capital

Before you decide what to invest in, you must know why you’re investing at all. This step is often skipped, especially by beginners eager to start buying. But placing trades without clarity is like setting off on a road trip without a destination. You might enjoy the drive at first, but eventually, you’ll run out of gas—or end up somewhere you never intended to go. A solid investment strategy starts with honest self-reflection. It requires asking questions that go beyond numbers and touch on life goals, emotional comfort, and personal values.

Begin by defining your primary objective. Are you saving for a child’s education, planning for early retirement, or building a cushion for unexpected expenses? Each goal has a different timeline and risk profile. A college fund needed in eight years requires a different approach than a retirement account with 25 years to grow. Next, assess your risk tolerance—not what you think you can handle in theory, but what you’ve actually experienced in market downturns. If a 15 percent drop makes you anxious, a portfolio full of volatile stocks isn’t a fit, no matter how high the potential returns. Honesty here prevents future regret.

Another key factor is time horizon. The longer you can stay invested, the more room you have to ride out short-term swings. This doesn’t mean ignoring losses, but it does mean understanding that volatility is normal. A long-term investor views market dips not as disasters but as opportunities to buy quality assets at lower prices. Once these elements are clear—goals, risk tolerance, time frame—you can begin constructing a portfolio that aligns with them. This might include a mix of low-cost index funds, dividend-paying stocks, bonds, and cash reserves. The exact mix will vary, but the principle remains: strategy follows clarity, not the other way around. When you know your purpose, every investment decision becomes simpler, because you’re not chasing returns—you’re fulfilling a plan.

Risk Control: The Silent Guardian of Wealth

Most people focus on how much they can earn. Few think about how much they can afford to lose. Yet, protecting capital is just as important as growing it. Think of risk control as the foundation of a house. You don’t see it once the walls go up, but without it, the whole structure can collapse. In investing, risk isn’t just about losing money—it’s about losing control. When losses exceed what you can emotionally or financially bear, you’re likely to make rash decisions. That’s when small setbacks turn into long-term damage.

One of the most effective tools for managing risk is position sizing—limiting how much you invest in any single stock or sector. For example, allocating no more than 5 to 10 percent of your portfolio to one company ensures that even if it fails completely, your overall wealth isn’t destroyed. I learned this the hard way. Early in my journey, I put nearly 25 percent of my portfolio into a single tech stock that seemed unstoppable. When the sector faced regulatory scrutiny, the stock dropped 60 percent in months. The financial hit was painful, but the emotional toll was worse. I felt foolish and shaken. After that, I set strict rules: no single stock above 8 percent, and no sector making up more than 25 percent of my holdings. These limits gave me peace of mind, even during turbulent times.

Diversification is another pillar of risk control. But true diversification goes beyond owning multiple stocks. It means spreading investments across different asset classes—stocks, bonds, real estate, and cash. It also means considering global exposure, not just domestic markets. When one region struggles, another may thrive. Holding a mix of these assets reduces the impact of any single downturn. Additionally, keeping a portion of your portfolio in cash isn’t a sign of fear—it’s a strategic choice. Cash provides liquidity during emergencies and buying power when opportunities arise. During the 2020 crash, those with cash reserves could buy优质 assets at discounted prices, while others were forced to sell at a loss. Risk control isn’t about avoiding all danger. It’s about managing exposure so you can stay in the game for the long run.

Smart Execution: Turning Ideas into Action Without Overthinking

Having a plan means nothing if you can’t follow through calmly and consistently. Many investors fail not because their strategy is flawed, but because their execution is emotional. They buy when prices are high and optimism is rampant, then sell when fear takes over. This pattern—buying high and selling low—is the exact opposite of what builds wealth. The key to breaking this cycle is developing a disciplined approach to buying and selling that removes emotion from the equation.

One of the most reliable methods is dollar-cost averaging. Instead of trying to time the market—guessing when prices will bottom or peak—you invest a fixed amount at regular intervals, regardless of market conditions. Over time, this means you buy more shares when prices are low and fewer when they’re high, resulting in a lower average cost per share. For example, investing $500 a month into a broad market index fund allows you to benefit from both up and down markets without needing to predict either. This method is especially effective for those with steady incomes who want to grow wealth gradually.

Equally important are clear entry and exit rules. Before buying any investment, define your reasons and set conditions for when you’ll sell. Is it a target price? A change in the company’s fundamentals? A shift in your personal goals? Writing these down helps prevent impulsive decisions later. I once held onto a declining stock far too long because I refused to accept I’d made a mistake. I had no exit plan, only hope. Now, I review each holding annually and ask: Does this still fit my strategy? If not, I sell without guilt. Finally, pay attention to costs. High fees from active funds, frequent trading, or expensive platforms eat into returns silently. Choosing low-cost index funds and tax-efficient accounts can save thousands over time. Smart execution isn’t flashy, but it’s powerful. It turns intention into results.

Learning from Mistakes: What the Market Taught Me the Hard Way

No investor gets it right all the time. The difference between those who succeed and those who struggle isn’t perfection—it’s how they respond to mistakes. I’ve made my share: chasing hot stocks, ignoring warning signs, and overestimating my ability to predict outcomes. Each error cost me money, but more importantly, it cost me confidence. What helped me recover wasn’t luck. It was reflection. I started keeping an investment journal, writing down every trade, my reasoning, and how I felt. Over time, patterns emerged. I saw that my worst decisions happened when I was afraid of missing out or trying to recover losses quickly.

One of the most painful lessons came from ignoring valuation. I bought shares in a popular consumer brand because everyone loved the product. The stock had already doubled in a year, and analysts were bullish. I told myself it was a long-term winner. But I didn’t ask: Is it fairly priced? Within months, growth slowed, and the stock dropped 40 percent. I held on, hoping to break even. It took two years to recover. That experience taught me to evaluate price relative to value. A great company isn’t a great investment if you pay too much. Now, I use basic metrics like price-to-earnings ratios and compare them to historical averages before buying.

Another mistake was overconfidence after a few wins. I had three successful trades in a row and started believing I had a “knack” for picking winners. I increased my risk, traded more frequently, and ignored my own rules. The market humbled me fast. A single bad bet erased months of gains. That was the moment I accepted: investing isn’t about being right all the time. It’s about being right enough, over time, by following a sound process. Mistakes aren’t failures if you learn from them. They become part of your wisdom. Every loss, if examined honestly, can strengthen your discipline and refine your approach.

Staying the Course: Consistency, Patience, and Long-Term Gains

The most powerful force in investing isn’t genius or luck—it’s compounding. When returns generate their own returns over time, small, consistent gains grow into something remarkable. But compounding only works if you stay invested. The temptation to react—to sell during fear or chase excitement during booms—breaks the chain. The real skill isn’t picking stocks. It’s maintaining calm and commitment through cycles you can’t control.

Think of investing like planting a tree. You don’t dig it up every time the weather changes. You water it, protect it, and let time do its work. The same is true with money. A well-structured portfolio, aligned with your goals and managed with discipline, will grow even when progress feels slow. During downturns, remind yourself why you started. Review your plan, not the headlines. Check your portfolio quarterly or annually, but avoid daily monitoring, which fuels anxiety. Routine, rational reviews keep you on track without triggering overreactions.

Patience isn’t passive. It’s active trust in your process. It means rejecting the myth that more action equals better results. In fact, the opposite is often true. Studies show that the average investor underperforms the market not because they pick bad funds, but because they trade too much, driven by emotion. Those who stay the course, rebalancing as needed but avoiding panic, consistently come out ahead. Success in investing isn’t about brilliance. It’s about clarity, consistency, and the courage to do nothing when the world screams to do something. When you build a strategy that reflects your life, your values, and your goals, you’re no longer gambling. You’re growing wealth with purpose—and that makes all the difference.