The Hidden Financial Risks of Remote Work Nobody Talks About

Working from home seemed like a dream come true—no commute, flexible hours, more control. But behind the comfort hides a new set of money traps I didn’t see coming. From blurred work-life boundaries affecting income to overlooked tax pitfalls and digital security threats, remote work reshapes not just your schedule, but your finances. I learned this the hard way, and now I’m sharing what I wish I knew earlier—so you don’t have to fall into the same holes. The truth is, the freedom of remote work comes with financial responsibilities that are easy to ignore until it’s too late. This article uncovers the hidden risks and offers practical steps to protect your income, savings, and long-term stability.

The Illusion of Stability in Remote Income

At first glance, remote work appears to offer steady income with fewer disruptions. Employees receive regular paychecks, and freelancers may land long-term contracts. Yet this surface-level stability can mask deeper financial fragility. Unlike traditional office roles that often come with structured benefits and longer notice periods, many remote positions operate in fast-moving, globalized markets where cost efficiency drives decisions. Companies can downsize or outsource entire teams with little warning, especially in sectors like tech, customer support, or digital marketing. For freelancers, demand fluctuates based on economic cycles, seasonal trends, or algorithm changes on freelance platforms—factors entirely outside their control.

One of the most dangerous assumptions remote workers make is that consistent monthly income equals long-term security. But income consistency does not guarantee job security. A sudden shift in company strategy, a drop in client budgets, or even a reorganization overseas can result in immediate termination. Unlike office-based employees who may benefit from workplace relationships or visibility, remote workers are often more anonymous and easier to replace. This lack of visibility can make it harder to advocate for oneself during restructuring. Additionally, many remote roles—especially contract or gig-based positions—lack health insurance, retirement contributions, or paid leave, leaving workers exposed to unexpected life events.

Signs of income instability are often subtle at first. These include delayed payments, reduced project frequency, last-minute schedule changes, or clients asking for discounts. When these patterns emerge, they signal a need for financial reassessment. Workers should treat such signals as early warnings, not isolated incidents. To mitigate risk, it’s essential to diversify income sources. This could mean taking on multiple clients, developing a secondary skill set, or creating passive income streams such as digital products or online courses. Relying on a single employer or platform increases vulnerability, especially during economic downturns when businesses prioritize cost-cutting. By recognizing that remote income is inherently more volatile, workers can take proactive steps to build financial buffers and reduce dependence on any one source.

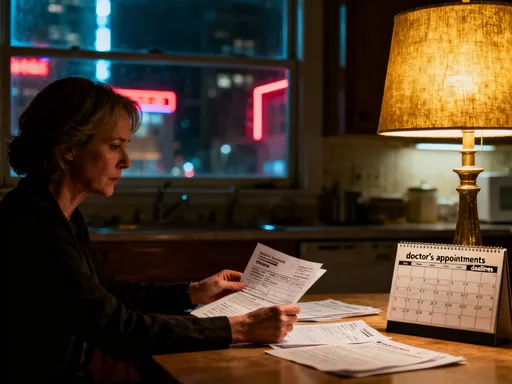

Tax Traps for Remote Workers Across Borders

Taxes are one of the most overlooked financial challenges for remote workers, particularly those who work across state or national lines. What seems like a simple change of location—working from a different city, state, or country—can trigger complex tax obligations. In the United States, for example, some states assert the right to tax income based on where the employer is located, not where the employee resides. This means a worker living in Texas but employed by a company in New York could be required to file and pay taxes in New York, even if they’ve never set foot in the state. These rules vary widely and can lead to unexpected tax liabilities if not carefully managed.

Digital nomads and international remote workers face even greater complexity. Many countries have strict rules about tax residency, often based on the number of days spent within their borders. Staying in a country for more than 183 days in a year can classify someone as a tax resident, making them liable for local income taxes. Without proper planning, individuals may end up paying taxes in both their home country and the country where they’re temporarily living—a situation known as double taxation. While some countries have tax treaties to prevent this, not all do, and the burden of compliance falls on the individual. Failing to report foreign income or misjudging residency status can lead to penalties, audits, or interest charges that erode hard-earned savings.

Another common mistake is missing out on legitimate deductions. Remote workers who use part of their home for work may be eligible for a home office deduction, but many don’t claim it due to confusion about eligibility or fear of triggering an audit. Others fail to track deductible expenses like internet bills, software subscriptions, or office equipment. Keeping detailed records and using digital tools to log workdays by location can help ensure accurate reporting. Consulting a tax professional who understands remote work is not just advisable—it’s a financial safeguard. A one-hour consultation could prevent thousands of dollars in unexpected taxes. The key is to address tax planning early, not during tax season when options are limited.

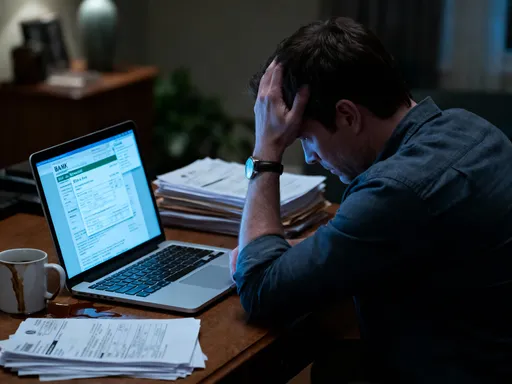

Cybersecurity Threats That Hit Your Wallet

Remote work increases exposure to cybersecurity risks, and the consequences go far beyond lost data. A single breach can lead to direct financial loss, damaged credit, legal fees, and even identity theft. Home networks are often less secure than corporate systems, making them attractive targets for hackers. Phishing emails, unsecured Wi-Fi connections, and weak passwords are common entry points. Once compromised, personal bank accounts, credit cards, and investment platforms can be accessed by criminals. In some cases, workers unknowingly install malware while performing routine tasks, giving attackers persistent access to sensitive information.

One of the most dangerous practices is using personal devices for work-related activities without proper protection. Many remote employees use the same laptop for checking personal email and accessing company systems. If that device is infected, it can expose both personal and professional data. In regulated industries such as finance or healthcare, employees may even face liability if a data breach occurs due to negligence. Some companies require workers to sign security agreements that hold them financially responsible for certain types of breaches. This means a single click on a malicious link could result in out-of-pocket costs for damages or regulatory fines.

The financial fallout from a cyberattack can be long-lasting. Victims may spend months resolving fraudulent transactions, disputing charges, and restoring their credit. Banks may freeze accounts during investigations, disrupting cash flow and causing missed bill payments. In extreme cases, stolen identities are used to open new lines of credit, leaving victims with debt they didn’t incur. Recovering from such damage requires time, effort, and often professional help—all of which come at a cost. To reduce risk, remote workers should use multi-factor authentication on all financial and work accounts, avoid public Wi-Fi for sensitive tasks, and maintain separate devices or user profiles for work and personal use. Investing in a virtual private network (VPN) and up-to-date antivirus software is not an optional expense—it’s a necessary layer of financial protection.

The Cost of Blurred Work-Life Boundaries

When your home doubles as your office, the boundary between work and personal life can dissolve quickly. Many remote workers find themselves checking emails late at night, answering messages on weekends, or working through meals. While this may seem like dedication, it often leads to burnout, reduced productivity, and hidden financial costs. The most immediate expense is time—time that could be spent on rest, family, or side projects that generate additional income. Over time, chronic overwork diminishes energy and focus, reducing overall earning potential.

Financially, the costs are both direct and indirect. Utilities such as electricity, heating, and internet rise when a home is used as a full-time office. These increases are rarely reimbursed by employers, especially for contract workers. Some individuals upgrade their internet plans, purchase ergonomic furniture, or invest in noise-canceling headphones—all necessary for productivity but often paid out of pocket. Unlike office workers who benefit from employer-covered overhead, remote employees absorb these expenses themselves. Over a year, these costs can add up to hundreds or even thousands of dollars, effectively reducing net income.

Another hidden cost is the erosion of personal time. When work expands to fill available hours, there’s less room for activities that support long-term financial health, such as learning new skills, managing investments, or planning for retirement. The “always-on” culture normalizes unpaid labor, where extra hours are expected but not compensated. This emotional labor—managing stress, maintaining availability, and performing constant self-regulation—takes a toll on mental health, which in turn affects job performance and career advancement. To protect against these costs, remote workers must establish clear boundaries. This includes setting fixed work hours, using time-tracking tools, and treating personal time as non-negotiable. Employers may not enforce these limits, but individuals must. Preserving personal time isn’t just about well-being—it’s a financial strategy that protects long-term earning capacity.

Investment Blind Spots in a Digital Workspace

One of the most significant financial disadvantages of remote work is the lack of access to employer-sponsored retirement plans. Traditional office jobs often include 401(k) options with employer matching—a benefit that effectively increases take-home pay. Remote workers, especially freelancers and independent contractors, typically don’t have access to such plans. Without automatic payroll deductions, saving for retirement becomes a manual, often neglected task. Many assume they can catch up later, but delayed contributions mean missing out on years of compound growth, which can result in a significantly smaller nest egg.

Another common issue is inconsistent investing. When income fluctuates from month to month, it’s easy to deprioritize retirement savings during lean periods. Unlike salaried employees who contribute a fixed percentage automatically, remote workers must initiate every transfer themselves. This reliance on willpower and consistency makes long-term financial planning more challenging. Some turn to high-risk side gigs to boost income, but these often lack stability and don’t contribute to sustainable wealth building. Without a structured approach, savings remain reactive rather than strategic.

To overcome these challenges, remote workers should establish automated savings systems. Opening an Individual Retirement Account (IRA) and setting up automatic transfers ensures consistent contributions regardless of income fluctuations. Even small, regular deposits grow significantly over time. Diversifying investments across low-cost index funds, bonds, and emergency savings reduces risk and creates a more resilient portfolio. The goal is to build a system that works without constant attention—because financial discipline tends to weaken under stress. Treating retirement savings as a non-negotiable expense, like rent or utilities, reinforces its importance. By addressing investment gaps early, remote workers can build long-term wealth without relying on employer benefits.

Overdependence on a Single Platform or Client

Many remote workers, especially freelancers, rely heavily on a single platform—such as Upwork, Fiverr, or Toptal—or a single major client for most of their income. While this can provide short-term stability, it creates a dangerous level of financial concentration. If the platform changes its fee structure, suspends accounts for policy violations, or experiences a drop in demand, income can disappear overnight. Similarly, if a key client reduces their budget, goes out of business, or decides to bring work in-house, the impact can be devastating. Unlike diversified businesses, those with a single revenue stream have little buffer against such shocks.

The risk is compounded by the lack of control. Platform algorithms determine visibility, pricing, and job access—factors that can change without notice. A freelancer with a five-star rating and hundreds of positive reviews can suddenly find themselves buried in search results due to an algorithm update. Clients may also consolidate their vendors, choosing to work with fewer providers. Without alternative income sources, workers face immediate financial pressure. Some respond by lowering rates to stay competitive, which further erodes profitability and makes recovery harder.

Diversification is the most effective defense. This means spreading client base across industries, building direct relationships outside of platforms, and developing multiple income streams. For example, a graphic designer might offer freelance services, sell digital templates, and teach online courses. Each stream provides a layer of protection. Regular income audits—reviewing where revenue comes from and how dependent one is on each source—can help identify overreliance before it becomes a crisis. Building an email list, maintaining a personal website, and networking independently of platforms increase resilience. The goal is not to eliminate platforms but to reduce dependence on them. Financial security in remote work comes not from maximizing short-term earnings, but from minimizing exposure to sudden disruptions.

Building a Resilient Remote Financial Plan

The path to long-term success in remote work isn’t about working more hours or chasing every opportunity. It’s about building a financial foundation that can withstand uncertainty. The first step is creating an emergency fund that covers at least six months of living expenses. This buffer provides peace of mind during income disruptions and prevents the need to take on high-interest debt. Funds should be kept in a separate, easily accessible account to avoid temptation and ensure availability when needed.

Insurance is another critical component. Health, disability, and liability coverage protect against unexpected events that could derail financial stability. Remote workers often overlook disability insurance, assuming they’re safe as long as they can work from home. But injuries, chronic conditions, or mental health issues can still impair the ability to perform job duties. Having income protection ensures continuity during recovery. For those using personal devices for work, cyber liability insurance may also be worth considering to cover potential breach-related costs.

Budgeting and regular financial checkups complete the framework. A clear budget tracks income, expenses, and savings goals, making it easier to spot trends and adjust behavior. Monthly or quarterly reviews help assess progress, update tax estimates, and evaluate investment performance. These habits foster awareness and control, reducing the likelihood of financial surprises. The ultimate goal is not perfection, but preparedness. By identifying vulnerabilities early—whether in income sources, tax compliance, or cybersecurity—remote workers can implement safeguards that preserve both freedom and financial health. Remote work offers incredible flexibility, but its rewards are fully realized only when protected by smart, proactive planning.